Thinking of buying a pre-owned car? These banks offer lowest interest

Compared to new cars, used car loans come with much higher interest rates. Depending on the lender, the difference can sometimes be as much as 5%

People are increasingly opting for personal mobility in the wake of the pandemic, as they wish to avoid crowded public transportation. However, a new car is often an expensive affair especially amid the pandemic, and many buyers feel that buying a used car would be a better option as a car is a depreciating asset.

It is possible to solve the mobility needs of an individual or a family in a cost-effective manner by considering a pre-owned car. In addition to the registration cost, you’ll also save on road tax, RTO fees, and other costs that have already been paid by the previous owner.

A majority of buyers opt for loans even when they buy used cars. Compared to new cars, used car loans come with much higher interest rates. Depending on the lender, the difference can sometimes be as much as 5%.

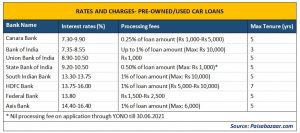

Some state-owned banks, such as Canara Bank, Bank of India, and Union Bank offer lower interest rates on pre-owned cars. The interest rates offered by these banks are quite competitive compared to those offered by other banks. Here is the list of banks offering the lowest interest rates:

List of banks that offer loans at low interest for pre-owned cars:

The lowest interest rate for a used car is offered by Bank of India at 7.35%-8.55% and by Canara Bank at 7.3%-9.9%, while Union Bank of India is third on the list with 8.9%-10.5% among public sector banks.

Among private lenders, South Indian Bank charges 13.3%-13.75% for pre-owned car loans, HDFC Bank at 13.75%-16%, and Federal Bank at 13.8%.

When it comes to pre-owned cars, banks and lending companies typically offer a five-year maximum tenure. However, HDFC Bank offers a maximum tenure of seven years while Bank of India’s loan comes with a minimum tenure of three years.