Freelancing with regular job? Know tax implications

The income of freelancers is taxable under the head ‘Profits and Gains of any Business or Profession’. They can file their return with ITR-3 or ITR-4.

A freelancer is a person who is self-employed and not working for a particular employer. The Covid-19 pandemic has increased the proportion of the workforce that performs freelance work. Along with their work, freelancers must not forget to take care of tax provisions to avoid any trouble in the future. Taking this into consideration, Tarun Kumar, chartered accountant and direct tax leader at Coherent Advisors highlighted some key points that every freelancer can keep in mind while managing their taxes.

Choosing the ITR Form

Many people who were earlier into jobs have turned to freelance work. Salaried class people usually file the return of income in form ITR-1. Income can be taxed as salary only if there is an employee and employer relationship. The income of freelancers is taxable under the head ‘Profits and Gains of any Business or Profession’. Thus, they can file their return of income in the form ITR-3 or ITR-4.

“The Income-tax Act also allows a freelancer to compute income from business or profession on a presumptive basis. The person having business income have to file a return of income in Form ITR-3. However, if the taxpayer has opted for a presumptive taxation scheme, he can file an income tax return in form ITR 4. The filing in Form ITR-4 is quite simpler whereas it is tedious and complex to file ITR-3. It is important to choose the correct ITR form else the return may become defective,” Kumar said.

Requirement to file ITR

The filing of an Income-tax return by the personal taxpayer is mandatory if his income before allowing capital gain exemption and deduction under Chapter VI-A exceeds the maximum exemption limit.

Even if income is below the exemption limit, the filing of return is mandatory if he has overseas assets, he deposited more than Rs. 1 crore in bank account, his foreign travel expense is more than Rs 2 lakh or electricity consumption is more than Rs 1 lakh.

Method of Accounting

The business profits are computed according to the method of accounting regularly employed by the assessee. A taxpayer can follow either a mercantile system of accounting or cash basis of accounting. Thus, if the assessee follows cash system of accounting, profits shall be computed on receipts basis, while in mercantile system, it should be computed on an accrual basis.

Computation of business income

The assessee needs to maintain the books of accounts with pieces of evidence that would enable him to compute the taxable income. While computing the business income, the expenses incurred, wholly and exclusively, for earning such income, can be deducted from this income.

For example, the freelancers working out of co-working spaces can claim a deduction of rent paid, telephone expenses, internet subscription or marketing expenses etc.

“There is no exhaustive list of expenses that can be claimed. If an item of expenditure is incidental to business or profession, it may be claimed as a deduction. The deduction can be claimed for the revenue expenditures. The capital expenditure, even if incurred to earn such income, is not deductible while computing taxable income. If an asset is acquired and used for his business or profession, then the depreciation can be claimed on such asset as per the rates prescribed under Income-tax Act,” Kumar pointed.

For example, the laptop used for freelancing work is eligible for depreciation at the rate of 40% every year on the written down value of such laptop.

Option of presumptive taxation scheme

Income-tax Act allows specified taxpayers to calculate and pay tax on a presumptive basis. This scheme was introduced to reduce the burden of compliances for small taxpayers.

“Taxpayers engaged in a business can opt for a presumptive scheme under Section 44AD if the turnover from the business doesn’t exceed Rs 2 crores. The income is computed at 8% of gross turnover. If business receipts are in digital mode then income is presumed to be at 6% of such digital receipts,” Kumar explained.

For professionals, he further added, “A presumptive taxation scheme is available under section 44ADA, provided the gross receipts from the profession do not exceed Rs 50 lakhs. The 50% of the gross receipts from such profession is deemed as presumptive income of the year.”

A person opting for the presumptive taxation is deemed to be have claimed deduction of all expenses. Any further claim of the deduction is not allowed after declaring the income at the rate of 6%/8%/50% of sales as the case may be.

Audit of books of accounts

A taxpayer who isn’t opting for a presumptive taxation scheme under Section 44AD is required to get his accounts audited if the turnover from business exceeds Rs 1 crore during the financial year. For professionals, it shall be mandatory if gross professional receipts exceed Rs 50 lakhs.

The tax audit can be conducted by a chartered accountant in practice. The purpose of a tax audit is to ensure that the taxpayer has maintained proper books of account and complied with the provisions of the Income-tax Act.

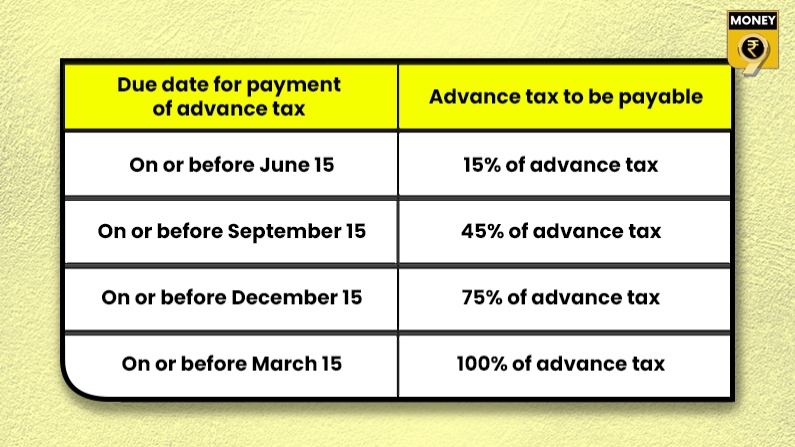

Payment of Advance Tax

Advance tax is required to be paid in the year in which the income is earned. Assessee is liable to pay advance tax if his estimated tax liability of the financial year is Rs. 10,000 or more. The advance tax, as per Kumar, shall be payable by the assessee in four instalments on or before the prescribed due dates as specified in the below table:

“However, unlike other taxpayers where tax is payable in four instalments, the assessee opting for presumptive taxation can pay the entire advance tax due for the financial year on or before March 15 i.e. if you are a taxpayer opting for a presumptive taxation scheme, you can pay for 100% of the advance tax in a single instalment up to 15th March,” he added.

TDS on freelancing income

The income earned by freelancers is subject to deduction of TDS. The payer is required to deduct tax on such income at the prescribed rates. Any person who is entitled to receive any income on which tax is deductible at source, he is required to furnish his PAN to the deductor. In case the PAN is not furnished, the tax shall be deducted at a higher rate.

“You should collect Form 16A (TDS certificate) from the deductor every quarter for taxes deducted by him and reconcile it with your Form 26AS which has details of TDS, TCS, Advance-tax and Self-assessment tax against your PAN. A taxpayer should always insist on the deductor for issuing the Form 16A downloaded from the income-tax website. If there is any mismatch in Form 16A issued by the deductor and the actual records, the taxpayer should ask the deductor to file the necessary corrections and issue the updated form 16A,” Kumar suggests.

Doing freelancing with regular job?

If you have earned freelancing income along with your regular job, then you need to aggregate both the incomes to compute the tax liability. If there is any deficit in the taxes deducted, then you need to pay the shortfall as self-assessment tax before the filing of the return. However, if the amount of TDS exceeds the actual tax liability, such excess amount can be claimed as a refund by filing an Income-tax return.

Claim Foreign Tax Credit (FTC)

“The world is turning digital and many online platforms help Indians to secure freelancing work from overseas. If the tax has been deducted outside India by a foreign entity on income earned from overseas, the Indian tax resident can claim FTC of such taxes as per the Double Taxation Avoidance Agreements entered into by the Indian Government with various countries,” Kumar asserted.

To claim the foreign tax credit in India, the taxpayer is required to submit Form 67 at the e-filing portal. It has to be filed on or before the due date of filing of the Income-tax Return.

Download Money9 App for the latest updates on Personal Finance.