This bond offers ‘optimal’ returns in fluctuating interest regime

Why are experts recommending dynamic bond funds? How do dynamic bond funds work, and are they for you? How is the current bond market favoring these debt funds?

Recently, in December’s Monetary Policy, the RBI’s Monetary Policy Committee (MPC) held the policy repo rate unchanged at 6.5% and retained the policy stance as ‘withdrawal of accommodation.’

As per many experts, the move was touted as a policy tone being very well balanced. As the RBI kept the repo rate unchanged, financial experts recommend adding a dynamic bond fund to balance risks and returns in your portfolio.

Let’s understand what they are and should you invest in dynamic bond funds:

The dynamic bond fund falls under the category of Debt mutual funds. As implied by their name, the composition and maturity profile of dynamic bond schemes are dynamic.

The primary objective of dynamic bond funds is to generate “optimal” returns in both rising and falling interest rate scenarios.

Under this fund, the fund manager keeps changing the portfolio based on the changing interest rates. This lets the fund offer steady returns no matter what happens to interest rates.

How do dynamic bond funds work?

Dynamic bond funds’ inherent flexibility allows them to quickly transition between long-, medium-, and short-term securities.

If the fund manager anticipates a decline in interest rates, he parks money in securities with longer maturities to take advantage of rising bond prices at the longer end.

On the other hand, if he believes that interest rates will increase, he can shorten the length of the portfolio by choosing bonds with shorter maturities.

Dynamic bond funds are viewed as year-round investments due to their potential to profit from rate changes in either way.

Taxation Dynamic bond funds are taxed as a debt mutual fund. Debt fund investments will no longer be eligible for the LTCG indexation benefit as of April 1, 2023. Instead, the investor’s gains will be taxed as part of their taxable income. No matter how long debt fund units were held, all profits on newly purchased units after April 1, 2023, will be considered STCG.

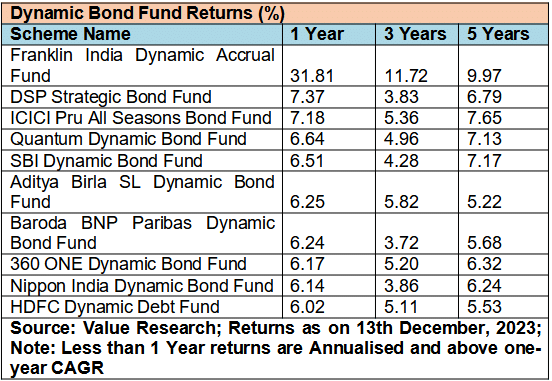

Returns

As per Ace mutual fund, the Dynamic Bond fund has given an average return of 7%,5%, and 6% over 1,3 and 5 years, respectively, as of December 13, 2023.

Should you invest?

One of the biggest advantages today of investing in debt mutual funds compared to traditional guaranteed fixed deposits is the faster transition of the interest rates, i.e., rate change by the banks and RBI.

Debt funds such as Dynamic bond funds show real-time reflection when interest rates rise or fall, making them a suitable option for investors.

Market experts believe that dynamic bond funds are currently in a good position to benefit from any future decline in inflation during the next one to two years.

Investors with a 2-3-year time horizon can consider dynamic bond funds in the mutual fund portfolio for their fixed income allocation.

Dynamic bond funds’ flexibility to change the portfolio positioning per the evolving market conditions makes them suited for long-term investors in this volatile macro environment.

Conclusion

There is a misconception that, as an investor, you can only benefit from debt mutual funds when the interest rate is falling. A product such as Dynamic bond fund can be an all-seasoned fund for your portfolio.

With the way interest rates are right now, investors can take advantage of higher rates while reducing risks related to market swings by putting their money into different types of debt.

Download Money9 App for the latest updates on Personal Finance.