Here’s why your car insurance premiums rise every year

The primary reason behind an annual increase in the car insurance premium is the rise in third party insurance premium rates by the IRDAI.

While it’s important to renew one’s car insurance on time, what can really irk you is the annual elevation in the premium costs. At every renewal, policyholders may tend to have paid a higher premium price for the same coverage. Have you pondered over why it happens? Especially after experiencing the usual reduction in the car value due to depreciation?

The primary reason behind an annual increase in the car insurance premium is the rise in third-party insurance premium rates by the Insurance Regulatory and Development Authority of India (IRDAI). For the unversed, as per the Motor Vehicles Act 1988, any car plying on public roads in India has to mandatorily be covered by a third-party cover, if not comprehensive car insurance.

How third party insurance contributes to higher premium?

The IRDAI determines the third party insurance premium rates for all cars. At the end of every financial year, the IRDAI evaluates the loss ratios of motor insurance companies vis-a-vis the total number of claims raised by car owners. After reviewing such factors, the insurance regulatory body declares the third party premium rates for the next financial year. In accordance with the Motor Vehicles Act, it is mandatory to have third party insurance for plying a vehicle on the road.

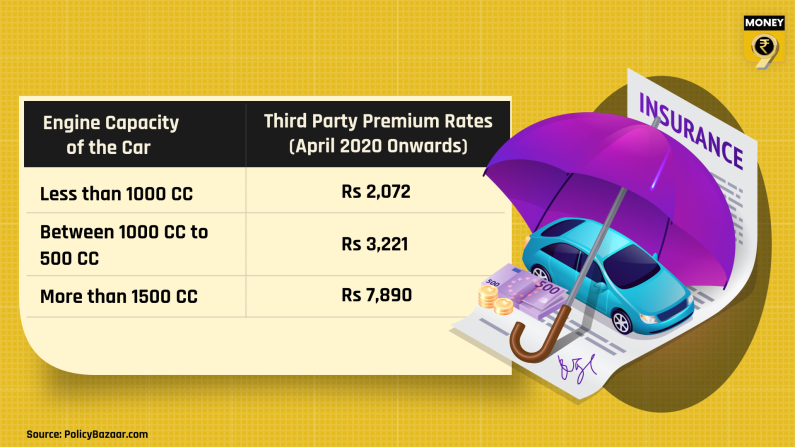

The above table displays third party insurance premiums rates for the financial year starting in April 2020. These rates will remain unchanged until the IRDAI directs any further.

Other factors responsible for higher premium?

While premium rates may differ from insurer to insurer, certain factors remain constant in determining these from the insurance company’s perspective. For example, the claim history plays a vital role in understanding whether the driver is risky or not. If multiple claims have been filed by you in the past year, the insurer sees you as a bigger liability and would charge a higher premium compared to those with no major claim history.

If your car insurance policy lapses due to non-renewal, buying a new plan can cause you to pay higher premiums than the existing sum. This is completely avoidable if you’re attentive enough to pay regular premiums and renew the policy on time.

At the same time, factors like type and age (brand new cars cost higher premium rates than older cars due to no depreciation) of the car will also impact the overall premium rates. The premium for luxury cars is more than that of a compact car as the former is more expensive with costly spare parts. Besides, the premiums are also higher for discontinued cars as fetching their spare parts is expensive.

How does Insured Declared Value trigger premium rates?

Meanwhile, there is a major possibility of your vehicle being inspected in case the policy renewal takes place after the significant gap. It can irk the insured and create unnecessary hassles. On top of that, any car damage found during such an inspection can lead to reduced Insured Declared Value (IDV) as well.

The IDV is the maximum claim amount which the insurer is liable to pay you in case of a total loss. Thus, higher IDV means the insurer will have to pay a higher claim amount and hence, the car insurance premium is higher for cars with a higher IDV and vice versa.

Ways to reduce car insurance premiums?

One smart way to lower your car insurance premium is to maintain the No Claim Bonus (NCB) which is a reward given by an insurance company to the policyholder for not raising any claim requests during a policy year. The NCB is a discount ranging between 20%-50% depending on the policy year and is given to the insured while renewing a policy. You can also avoid raising claims for minor defaults as each one counts as the time of renewal. Even add-on covers should be included after careful introspection. Not every add-on may be required for your vehicle.

Most importantly, renew your car insurance on time. Most people tend to enthusiastically buy comprehensive car insurance and/or third-party cover while purchasing the car. However, it’s equally important to renew the insurance plan within the stipulated timeline. On-time renewal saves you from any kind of legal or financial implications and saves both time and mental stress.

Download Money9 App for the latest updates on Personal Finance.