Should you invest in banking and PSU debt funds?

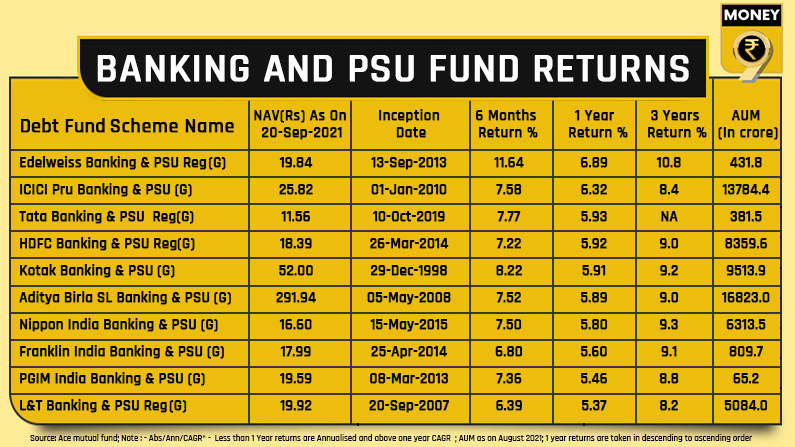

The returns achieved by the majority of banking and public sector debt funds averaged 5.51% on the amount invested in the last one year

Given the uncertainty surrounding interest rates and liquidity, mutual fund experts feel that the future for banks and public sector fund schemes remains favourable. Banking and public sector debt funds have given a return of 5.38%, 8.56%, and 7.57% in the last one, three, and five years shows the Value Research data as of 20th September 2021.

Banking and public sector undertaking mutual funds are required to invest at least 80% of their assets in debt instruments issued by banks, public sector undertakings, and public financial institutions.

That said, to develop the portfolio, fund managers primarily focus on Maharatna and Navratna companies, which have a track record of generating high returns. Due to the investing universe and the fact that most entities are owned by the government, investment experts consider these schemes to be safer investments.

The returns achieved by the majority of banking and public sector debt funds averaged 5.51% on the amount invested in the last one year. (See the returns table below)

What are the limitations?

-Low returns: Debt securities earn less than equity investments. Additionally, because a PSU and banking debt fund’s investment portfolio consists primarily of debt securities issued by large-cap corporations, the likelihood of a significant increase in stock prices is minimal. Thus, revenues realised, while certain, may be limited.

-Further banking and PSU funds have a holding period of between one and three years. As a result, it is not a good vehicle for investors seeking reliable long-term investment opportunities.

Taxability aspect

After three years, investors who earn capital gains on the sales of banks and PSU fund net asset value (NAV) units are taxed on the gain as LTCG (long-term capital gains). After indexation, a 20% LTCG tax is imposed on total earnings realised.

Who should invest?

Due to the Reserve Bank of India’s and the central government’s strict regulation and oversight of banks, many investors believe they are generally safe even during times of crisis.

If you’re seeking somewhat safe debt mutual fund investments with a three-year or longer investment horizon, you may want to invest in these schemes. They may provide you with a higher rate of return after taxes than standard bank fixed deposits.